It makes sense to own a property now…a look at some reasons why this particular option could even be the best form of investing for a salaried individual

Rising cost of living

There is a difference between investment and savings. Savings just compensates partial cost of inflation while does not give appreciation over inflation. Examples of savings are fixed deposit,postal savings etc. for example if Mr.X has Rs.100 and wants to buy a chocolate for himself and his son but when he goes to shop he realises he cost of chocolate is Rs.100 for single piece he goes to post office or bank and deposits Rs.100 to wait till it becomes Rs.200 i.e around 10 years. When his savings mature he withdraws Rs.200 and goes to same shop keeper to realise the cost of chocolate is now Rs.300 per piece. This is savings.

Investment on the other hand carries risk of time lesser the time more the risk. Without time it becomes gamble where immediately either it appreciates or depreciates. Though it carries the risk of time it can only beat the inflation and give reasonable return over inflation if planned properly. Investment is now not choice but compulsion looking at the rising cost of living your retirement or later years needs planning now and earlier done the better it is.

Imagine yourself in 2036. For that you need to be future focus.

→ Are you future-focused or present-focused? The marshmallow experiment.

What I’m about to tell you is one of the most interesting things I’ve read or heard in the last few months, and I know you’re going to love it, so please read to the end.

The Marshmallow Experiment

40 years ago, at a nursery school at Stanford University, psychology professor Walter Mischel ran an experiment.

A bunch 4-year-olds were brought into a room, one at a time. They were given one marshmallow, and told they were allowed to eat it immediately, but if they could wait 15 minutes without eating it, they’d be given a second marshmallow, and could eat both.

70% of the kids ate the marshmallow right away. Only 30% of the kids could wait the full 15 minutes to get the second marshmallow. This experiment has been repeated in other countries (Brazil and Japan) over the years, and the ratio stays the same: two-thirds can’t wait, one-third wait.

But here’s the interesting part:

15 years later, the researchers followed-up and found that those kids who waited for the second marshmallow scored, on average, 250 points higher on the SAT test, and were higher achievers in whatever field they had chosen (academic, athletic, artistic). They were all-around more successful and happier.

So the ability to delay gratification is one of the best indicators of future success.

Your Time Focus

So what are you really doing when you delay gratification?

You’re giving more importance to the future than the present. Willing to give up a little pleasure in the present, to benefit your future self.

The great book, The Time Paradox, notes that we all have a different time-focus that greatly shapes how we think and act.

Future-Focused People

For future-focused people, long-range goals fuel today’s decisions and actions. This keeps them ambitiously working, saving, and planning for a better life. Self-discipline and the ability to delay gratification are key.

Future-focused people are more successful professionally and academically. They also eat well, exercise regularly, and schedule preventative health exams.

But by always looking through the present to the next goal, they often do not fully appreciate the present. Think of the stereotype of the successful executive who is always too busy for his family. (Friends and family require your attention to be in the present.)

Present-Focused People

Present-focused people actively seek activities and relationships that bring pleasure, variety, immediate gratification, and short-term payoffs. They avoid anything tedious, requiring effort, maintenance, or routine. They’re playful and impulsive, engaging in leisure activities (until it becomes boring).

Present-focused people are more likely to gamble, use drugs and alcohol. They’re less likely to exercise, eat well, floss, or get regular health exams. They are the least likely to be successful.

While some present-focus is needed to enjoy life, too much present-focus can rob life of the deeper happiness of accomplishment.

Past Focus

How you view the past is also important because we see our lives as having a trajectory. If you remember the past as happy, you predict your future will be happy. If you are haunted by an unhappy past, you probably predict your future to be unhappy, too.

So what is your focus?… What will be your 2036? Or for that matter 2026? What cost of living do you expect? What will be your financial requirements or commitments? Have you planned it???….

| Necessary Goods/Services | 1985

(Price) |

2011

(Price) |

2021

(Price) |

| 1 Litre of Petrol | 8 | 67 | 140 |

| Toothpaste | 5 | 54 | 110 |

| 1 kg of sugar | 4 | 28 | 62 |

| 1 litre of milk | 4 | 32 | 70 |

| BhajiPav | 5 | 70 | 150 |

| Doctor fees | 10 | 100 | 250 |

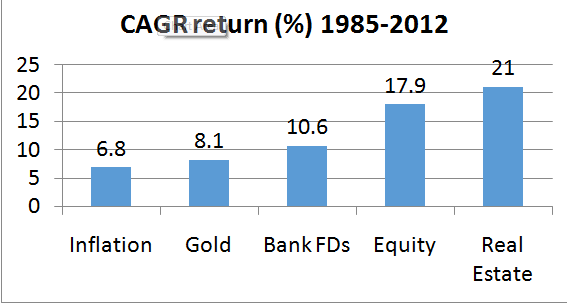

Most people with investable surpluses tend to stay focused on the financial markets,whether it is debt or equity. Very few venture into real assets such as gold or real estate. An investment in a second property(apart from your house) is an effective way to build wealth in the long-term.Let’s examine the various reasons why this could even be the best form of investing for a salaried individual.

Outlook for real estate

Real Estate prices in india have grown at between 20% to 30% annually, over the past 50 years, across regions and across various reasonably long(10 years or more) time frames. This growth is projected to continue,given the combination of various enabling factors. These include a favourable demographic distribution in the country,increasing urbanisation and an increasing preference for nuclear families, easy finance availability and most important evergrowing population india is estimated to become the worlds largest populous country in by 2022.

Such returns are comparable or even better to those in the equity capital markets with added security of physical asset in form of real estate.Infact, there is the additional advantage that one is spared the variability and risks associated with investing in equities. For example while the BSE sensex has multiplied 160 times since 1979, the components of the sensex have been changing constantly.

“Price is a function of Demand & Supply”-Adam Smith

( The Father of Economics)

Demand of Land

- 258 person/ sqk.m which is expected to go up to 412 in 2020

- 2074355 sq meter area land would be needed for Residential and Commercial Purpose

- GDP growth of more than 8.5% which gives further boost to demand as all activities require space to operate

- Purchasing power increase

- More than 50% of Indian Population is below age 25 which means there is huge demand for Residential Homes in future as they will settle

- Shift towards nuclear family

- Banks offers attractive interest rate which will further Boost demand.

- Per capita income is increasing

- It is also one of the source of parking cash money

Current approx. use pattern of land. Forest will be reserved by government, land can only be available from agriculture which also needs land in large quantity thus pushing the prices further

Decide Yourself

| Criteria | Fixed Deposit/ p.o | ULIP | Mutual Fund | Shares | Gold | Real Estate |

| Inflation Protection | NO | YES | YES | YES | YES | YES |

| Liquidity | YES | NO | YES (AT MARKET RISK) | YES (AT MARKET RISK) | YES (AT MARKET RISK) | YES( Through Mortgage/Sale) |

| Guaranteed Income | Yes | No | No | No | No | YES( incl of Rental Income) |

| Feel of Ownership | NO | NO | NO | NO | YES | YES |

| Form | Paper | Paper | Paper | Paper | Physical | Physical |

| Risk | Low | Medium | Medium | High | Low | Low |

| Probability of capital loss | No | Yes | Yes | Yes | Yes | No |

Tax efficiency factor

There are several tax advantage that can be availed by investing in a second property. These include:

Possibility of rental income in long run. Tax benefit in principal payment and interest component in tax. When the house is sold, the acquisition cost(adjusted for indexation) is deducted from the sale proceeds and only the balance is taxable, if the property is held for more than 3 years.

Ability to leverage

The purchase of a second home is one of the few form of investment for which leverage is available for salaried individuals. It is possible to invest in a second property by putting only 20% of the cost of the property as one’s equity, and take a loan for the rest. It can even be used for mortgage for security.

Financial Logic Involved

So then,the financial logic for investing in a second property is simple. Assume the following. You own the asset by paying only 20% of the cost. Your average cost of financing the remaining is less than 10%(interest rate of 9.55%). The rental yield and property appreciates by 20% every year.

To understand your financial situation every year, see the box below. As is evident, the return on the investment is quite healthy.

Annual Return on Investment

| ASSUMPTION | |

| Cost Of Propety | 500000/- |

| Investment(DP @ 20%) | 100000/- |

| Loan(5 Years @ 9.55% annual Int.) | 400000/- |

| Annual Appreciation | 20% |

Return on Investment

| Initial | Year1 | Year2 | Year3 | Year4 | Year5 | Year6 | Year7 | Year8 | Year9 | |

| Value of Property | 500000 | 600000 | 720000 | 864000 | 1036800 | 1244160 | 1492992 | 1791590 | 2149908 | 2579890 |

| Loan Outstanding | 400000 | 334454 | 262367 | 183086 | 95894 | 0 | 0 | 0 | 0 | 0 |

| Rent Received | 0 | 0 | 0 | 0 | 0 | 0 | 44790 | 47029 | 49381 | 51850 |

| Interest Paid on Loan | 0 | 35380 | 28839 | 21645 | 13734 | 5033 | 0 | 0 | 0 | 0 |

| Tax break Rec. | 0 | 25846 | 25846 | 25846 | 25846 | 25846 | 0 | 0 | 0 | 0 |

| Net Cash Outflow | 0 | -9534 | -2993 | 4201 | 12112 | 20813 | 44790 | 47029 | 49381 | 51850 |

| Annual Return on Investment | 0 | 32% | 43% | 51% | 56% | 60% | 62% | 61% | 61% | 61% |

Net Cash Outflow:-(Rent Rec.+ Tax bracket Rec.-Interest paid on loan)

Rent:-3% of Market Value of Starting Year & Hike by 5% every Year

Loan O/s &Interest :- Calculation of Interest and Loan outstanding component on the basis of existing norms of the bank.

Annual Return On Investment:- Investment as down payment is Rs 100000/- initially and very next year investment amount hike by 20% than investment is 120000/- .Further after one year total capital repayment to bank is 65546/- also earns hike of 20% than investment is 78655/- ,benefit from income tax-25846/-(120000+78655+25846)=224501 less interest paid-35380/-.(224501-35380)=189121. Accordingly total return on Investment is 189121/600000(Market Value of Same Year)=32%.

Tax Saving On Housing Loan

| Tax Saving on Houosing Loan | |||||

| Person having income of Rs 40000per month | If not having any loan arrangments (A) | If having Housing loan arrangments (B) | |||

| Gross Income | 600000 | 600000 | |||

| Deductions | Housing Loan Principal Repayment & Housing Loan Interest (8411*12) | NIL | 100932 | ||

| Taxable Income | 600000 | 499068 | |||

| Tax Liability | 46350 | 20504 | |||

| Yearly Tax Savings (A) – (B) | 25846 | ||||

| If you are taking Loan of Rs4Lacs @ 9.55% Interest Rate for 5 Years then monthly Installment would be8411 | |||||

| Your Total Interest Component for 5 years would be | 104631 | ||||

| Your Tax Savings in 5 years 25846*5) | 129230 | ||||

| Tax Saving due to Housing Loan Arrangment | 24599 | ||||

There’s a flip side

There are some factors that one needs to know before buying a second property. You should be comfortable with the monthly instalment to be paid over the long term. Additionally, purchase of property entails a thorough evaluation of the developer, his track record and other legal aspects of the property.It is very important that developer will be backing the project till the end is strong enough to do so. legal aspects can be taken care by banks in case of loans as loans will be available in completely legal properties only. In summary, a second property is a worth while investment, especially for the salaried class it is an efficient way to build wealth in the long term.

Asset Class Return